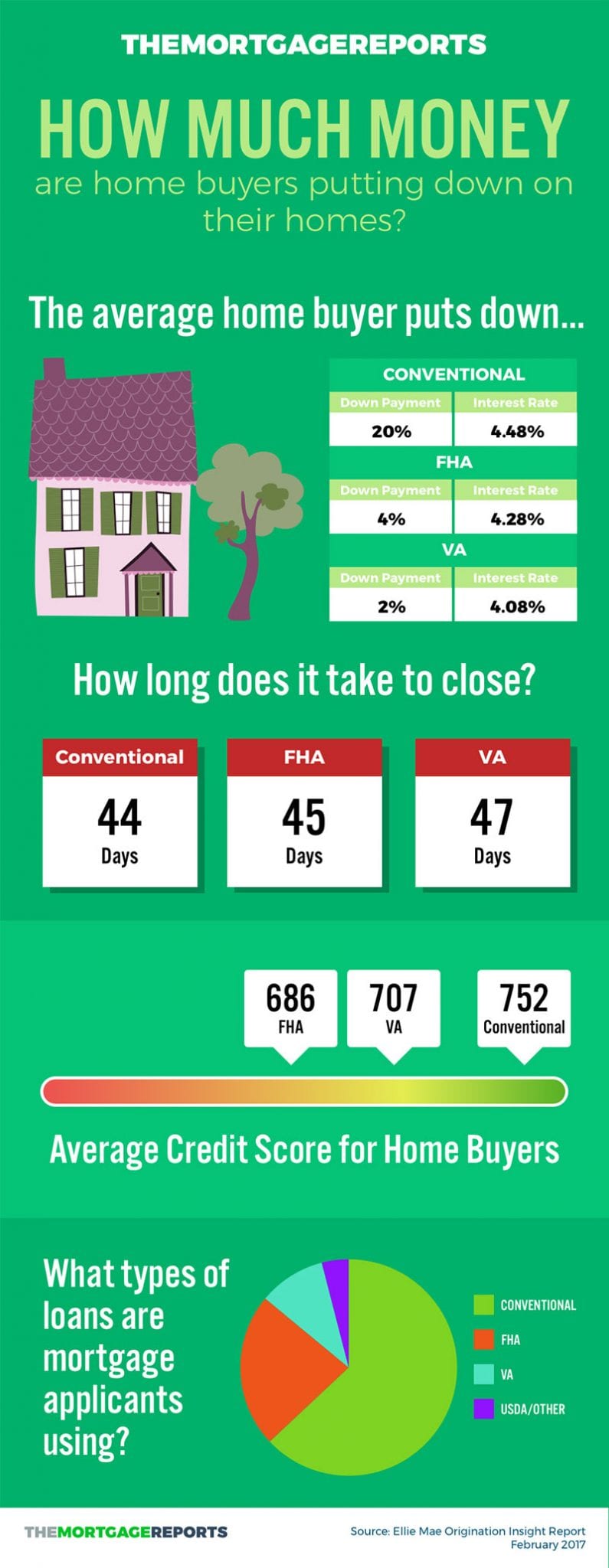

There Is No “Good” Or “Bad” Downpayment Level

Choosing the right loan type is an important part of home buying. There are many different mortgage options available, and each comes with its own set of benefits.

But when choosing a loan type, don’t overlook the importance of your downpayment.

The amount you put down will play a large role in your monthly payments, your mortgage rate, and how much home you can qualify for.

For some buyers, making a large downpayment makes sense. For others, there are options that require little or no downpayment.

There is no “good” or “bad” downpayment amount. It depends on the buyer’s situation and long-term goals.

Fortunately for home buyers, mortgage rates are at long-term lows. Homes are affordable no matter which downpayment option buyers choose.

Still, making a good decision about your downpayment is a key part getting the most value from your home purchase.

Verify your new rateZero-Down Options

Some loan types require a small downpayment, some require none at all. It would make sense if these loans came with sky-high interest rates and credit score minimums. Many home buyers are surprised to hear that these two programs offer lower rates than some 20% down loans.

Lower-credit borrowers are eligible, and lenders are eager to approve first-time and repeat buyers.

0% Down USDA Loans

USDA loans could be the right choice for those who want a home in a suburban or rural area.

The United States Department of Agriculture (USDA) backs this loan in an effort to promote homeownership and economic development in less-dense areas.

The Rural Development (RD) loan, as it is also known, is available to those buying in a “rural” area.

But don’t let the word “rural” concern you.

The definition of rural is quite generous. Many suburban areas just outside of major metro centers are within USDA home loan boundaries.

USDA loans offer 100 percent financing, so the buyer doesn’t need to put any money down on their home if they don’t want to.

Borrowers can have a credit score of 640. This is well below the credit score of the average home buyer across all loan types. The average buyer has a score around 720, according to loan software company Ellie Mae.

USDA loans come with less-expensive mortgage insurance than that of FHA. On a $250,000 loan, USDA mortgage insurance will save the buyer $625 annually compared to FHA.

This loan product probably has the least name recognition of any loan type, yet it’s growing in popularity as home buyers realize its benefits.

Verify your new rate0% Down VA Home Loan

Another popular zero-down loan program is the VA loan. The U.S. Department of Veterans Affairs (VA) offers this loan program to active military members and veterans of the U.S. armed forces.

This program is different from other government-sponsored programs in that there is no mortgage insurance required. A VA buyer will save more than two thousand dollars per year on a loan size of $250,000 versus an FHA buyer.

VA loans also carry the lowest mortgage rates of any loan type, typically around 0.25% below rates for conventional loans according to Ellie Mae.

Also, a VA loan has incredible flexibility. Lenders allow credit scores down to 620 or lower thanks to strong government backing. VA loans were created to make homeownership accessible and affordable for military members and veterans.

Home buyers with any military experience should check their VA loan eligibility before making a final decision on a loan program.

Low-Downpayment Options

Low downpayment loans are widely available from almost every lender in the country. With as little as 3% down, these loans drastically reduce the initial home buying cash investment.

3% Down Conventional 97

A low downpayment option that is gaining popularity is the Conventional 97 mortgage. The home buyer needs only 3% down, making the loan-to-value (LTV) ratio 97. This mortgage option requires a credit score of 620.

The conventional 97 loan requires PMI, but depending on your credit score, the mortgage insurance could be less expensive than that of FHA.

Those looking to keep the home and loan long term might opt for this loan; mortgage insurance automatically drops off when you build 22% equity in the home. FHA mortgage insurance remains for the life of the loan. Home buyers must refinance to cancel FHA mortgage insurance.

Because conventional PMI can be cancelled, buyers often opt for it, even when it is more expensive than FHA mortgage insurance.

3.5% Down FHA Loan

One of the most popular low downpayment options is the FHA loan. These mortgages are backed by the Federal Housing Administration (FHA) and require a credit score of just 580 and a downpayment as little as 3.5%.

FHA loans require a monthly mortgage insurance premium (MIP) payment. This is FHA’s “brand” of mortgage insurance and serves the same purpose as private mortgage insurance (PMI) on conventional loans. While mortgage insurance of any type means extra cost, it also means the buyer can put less money down and buy a home sooner.

An of $250,000 and the minimum down payment would require monthly FHA MIP of about $170 per month. In this example, paying MIP would reduce the buyer’s downpayment by about $40,000.

Low downpayments are not the only reason FHA loans are popular. because of their lenient requirements and low downpayment. Many home buyers will find that an FHA loan works best for them.

Verify your new rate5% To 10% Down Options

The minimum downpayment for a conventional loan is 3%. But you can make a larger downpayment.

Increasing your downpayment to just 5% can reduce your interest rate by about 0.125%. Conventional loan rates are based on a tiered system that adjusts rates for different downpayment and credit score levels.

Generally, the higher your downpayment and credit score, the lower your rate.

Home buyers who put at least 5% down on a conventional loan can also save on PMI. According to mortgage insurance provider MGIC, a borrower will save about $30 per month on a $250,000 loan by increasing the down payment to five percent.

But there are no rules against making an “odd numbered” downpayment percentage. Home buyers can make a downpayment of 6% or 7%. The reason most home buyers don’t, however, is that there are no rate or PMI savings at these mid-range downpayment levels.

More savings are available at the 10% down tier: PMI drops another $40 per month compared to the above five-percent-down example.

Verify your new rate10% To 20% Down, Or More

Many home buyers will opt to put down 20 percent, or even more, on their new home. The benefits of putting this much down are fairly straight-forward: the buyer can eliminate mortgage insurance, pay less interest, and enjoy a lower monthly payment.

But paying 20 percent of a home’s price upfront may not be the best option, even for borrowers with the cash to do so.

With mortgage rates as low as they are, it could make sense to accomplish other financial goals with that cash. Still, some buyers feel more comfortable making a large downpayment.

There is no “right” or “wrong” downpayment amount. It all depends on the buyer’s comfort level.

80-10-10 Mortgage

Many home shoppers want to put less than 20 percent down while avoiding monthly insurance payments. Fortunately, there are ways to get around monthly insurance.

The 80-10-10 loan, also known as the “piggyback” loan, lets the buyer put less than 20 percent down and avoid monthly insurance payments.

Piggyback loans are actually two loans opened up at the same time when buying a home. The first loan is for 80 percent of the home value, and a second loan worth 10 percent “piggybacks” on top of the first loan. The second, smaller loan is a second mortgage, which can take the form of a home equity loan or home equity line of credit (HELOC).

The second mortgage is sometimes offered by the lender of the first loan. However, buyers can also shop around for the “piggyback” portion of their mortgage with their local credit union or with online lenders.

Lenders consider your second mortgage as part of your total downpayment. This is why 80-10-10 loans eliminate the need for mortgage insurance.

Higher credit scores are typically required for a piggyback loan, but for many buyers, they are the right balance between making a substantial downpayment and avoiding mortgage insurance.

Verify your new rateConventional Mortgages At 20% Down Or More

Conventional mortgages are loans that are not backed by the government. Because downpayments are larger, mortgage lenders and the investors don’t need extra backing by government agencies or a mortgage insurance policy attached to the loan. This drives down costs for the home buyer.

These loans are a favorite of applicants who want to make a downpayment of twenty percent or more.

Sometimes, home buyers wish to make a downpayment of 50% or more. This reduces their overall payment drastically, and sets them up to eventually rent the home at a profit.

A conventional loan can also be used to buy a rental property or second home.

Buying a condo can also be much easier with a conventional loan, especially compared to FHA.

Examine your long-term goals. It could turn out that a large downpayment on a conventional loan fits your needs perfectly.

What Are Today’s Rates?

Mortgage rates are at ultra-low levels, no matter which downpayment option you choose. Get a rate quote based on your desired downpayment and loan type. Many home buyers are surprised at what they can afford at today’s rates.

Get a live rate quote, which comes with access to your credit scores. Very little information is required to start.

Time to make a move? Let us find the right mortgage for you